I have spent nearly a decade as a data scientist in the retail sector, but I have been approaching customer spend predictions the wrong way until I attended Gregory M. Duncan’s lecture. Accurately predicting how much an individual customer will spend in the next X days enables key retail use cases such as personalized promotion (determine X in Buy-X-Get-Y), customer targeting for upselling (which customers have higher purchasing power), and early churn detection (customers do not spend as much as they should). What makes this problem particularly difficult is because the distribution of customer spending is both zero-inflated and long/fat-tailed. Intuitively, most customers who visit your store are not going to make a purchase and among those who do, there will be some super customers who purchase an outrageous amount more than the average customer. Some parametric models allow for zero-inflated outcomes such as Poisson, negative binomial, Conway-Maxwell-Poisson; however, they do not handle the long/fat-tailed explicitly. Even for non-parametric models such as decision tree ensembles, more resources (trees and splits) will be dedicated to separating zeros and handling outliers; this could lead to deterioration in performance. Using the real-world dataset UCI Online Retail, we will compare the performance of common approaches namely naive baseline regression, regression on winsorized outcome, regression on log-plus-one-transformed outcome to what Duncan suggested: hurdle model with Duan’s method. We will demonstrate why this approach outperforms the others in most evaluation metrics and why it might not in some.

This Is Not a Drill: Real-world Datasets, Meticulous Feature Engineering, State-of-the-art AutoML

To make this exercise as realistic as possible, we will use a real-world dataset (as opposed to a simulated one), perform as much feature engineering as we would in a real-world setting, and employ the best AutoML solution the market has to offer in AutoGluon.

Code

online_retail = fetch_ucirepo(id=352) transaction_df = online_retail['data']['original']original_nb = transaction_df.shape[0]#create yearmon for train-valid splittransaction_df['yearmon'] = transaction_df.InvoiceDate.map(string_to_yearmon)#get rid of transactions without cidtransaction_df = transaction_df[~transaction_df.CustomerID.isna()].reset_index(drop=True)has_cid_nb = transaction_df.shape[0]#fill in unknown descriptionstransaction_df.Description = transaction_df.Description.fillna('UNKNOWN')#convert customer id to stringtransaction_df['CustomerID'] = transaction_df['CustomerID'].map(lambda x: str(int(x)))#simplify by filtering unit price and quantity to be non-zero (get rid of discounts, cancellations, etc)transaction_df = transaction_df[(transaction_df.UnitPrice>0)&\ (transaction_df.Quantity>0)].reset_index(drop=True)has_sales_nb = transaction_df.shape[0]#add salestransaction_df['Sales'] = transaction_df.UnitPrice * transaction_df.Quantity

We use the UCI Online Retail dataset, which contain transactions from a UK-based, non-store online retail from 2010-12 and 2011-12. We perform the following data processing:

Remove transactions without CustomerID; from 541,909 to 406,829 transactions

Filter out transactions where either UnitPrice or Quantity is less than zero; from 406,829 to 397,884 transactions

Fill in missing product Description with value UNKNOWN.

We formulate the problem as predicting the sales (TargetSales) during Q4 2011 for each customers who bought at least one item during Q1-Q3 2011. Note that we are interested in predicting the spend per customer as accurately as possible; this is common for marketing use cases such as determining what spend threshold to give each customer in a promotion, targeting customers for upselling, or detecting early signs of churns. It is notably different from predicting total spend of all customers during a time period, which usually requires a different approach.

Code

feature_period = {'start': '2011-01', 'end': '2011-09'}outcome_period = {'start': '2011-10', 'end': '2011-12'}feature_transaction = transaction_df[(transaction_df.yearmon>=feature_period['start'])&\ (transaction_df.yearmon<=feature_period['end'])]outcome_transaction = transaction_df[(transaction_df.yearmon>=outcome_period['start'])&\ (transaction_df.yearmon<=outcome_period['end'])]#aggregate sales during outcome periodoutcome_sales = outcome_transaction.groupby('CustomerID').Sales.sum().reset_index()#aggregate sales during feature periodfeature_sales = feature_transaction.groupby('CustomerID').Sales.sum().reset_index()#merge to get TargetSales including those who spent during feature period but not during outcome (zeroes)outcome_df = feature_sales[['CustomerID']].merge(outcome_sales, on='CustomerID', how='left')outcome_df['Sales'] = outcome_df['Sales'].fillna(0)outcome_df.columns = ['CustomerID', 'TargetSales']

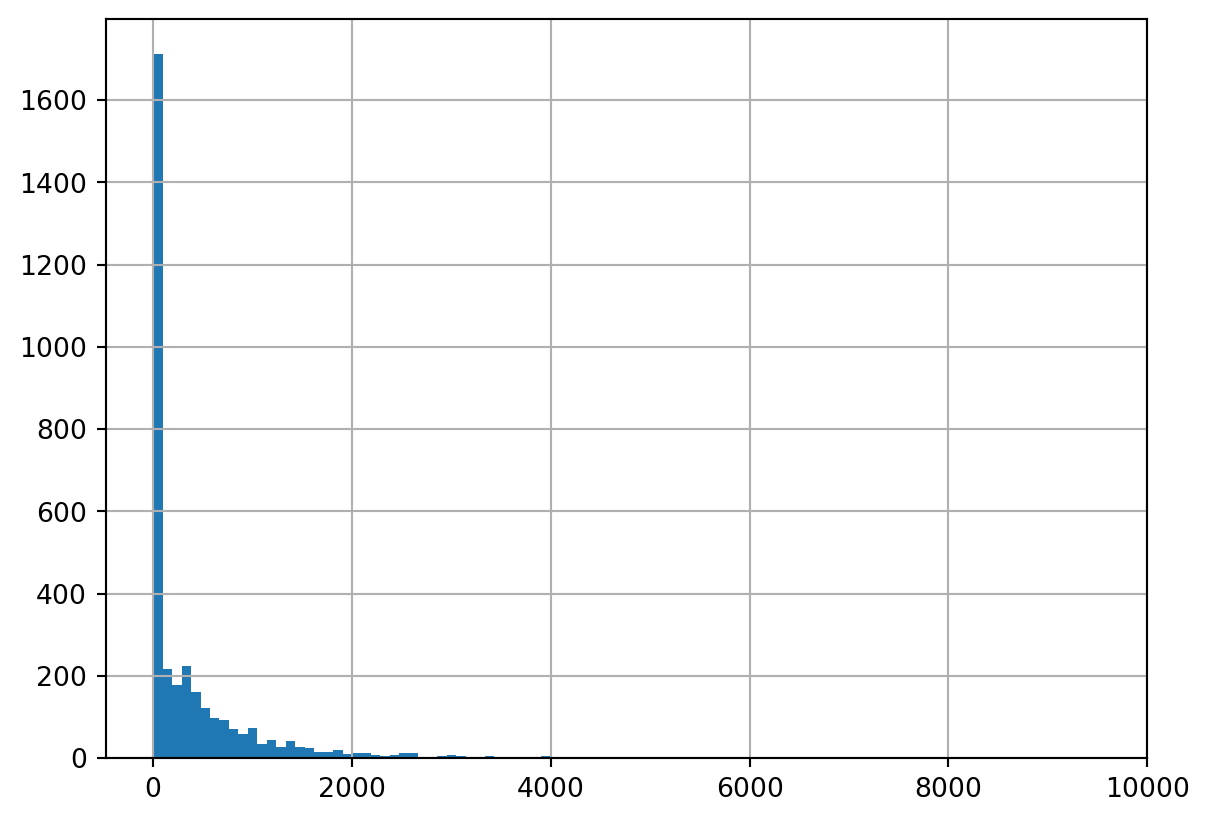

We transform the transaction dataset into a customer-level dataset where we calculate features using transactions between 2011-01 to 2011-09 and outcome using transactions between 2011-10 to 2011-12, summing Quantity times UnitPrice. We left-join the customers in feature set to outcome set. This will result in the zero-inflated nature of the outcome as not all customers will come back in Q4. The distribution of non-zero sales is naturally long/fat-tailed with a few customers having extraordinarily high amount of sales in Q4. This resulted in a customer-level dataset with 3,438 customers.

Code

#confirm zero-inflated, long/fat-tailedoutcome_df.TargetSales.describe(percentiles=[i/10for i inrange(10)])

We represent a customer using traditional RFM features namely recency of purchase, purchase days, total sales, number of distinct products purchased, number of distinct category purchased, customer tenure within 2011, average purchase frequency, average purchase value, and percentage of purchase across all 9 categories. This is based on data from Q1-Q3 2011.

Since the UCI Online Retail dataset does not have a category but only contains descriptions over 3,000 items, we use LLaMA 3.2 90B to infer categories based on randomly selected 1,000 descriptions. This is to make the category preference representation for each customer, which is more tractable than including features about all 3,548 items. After that, we use Claude 3.5 v2 to label a category for each description as it performs structured output a little more reliably. The categories are:

Home Decor

Kitchen and Dining

Fashion Accessories

Stationary and Gifts

Toys and Games

Seasonal and Holiday

Personal Care and Wellness

Outdoor and Garden

Others

Code

descriptions = feature_transaction.Description.unique().tolist()print(descriptions[:5])#randomize descriptions with seed 112 to get which categories we should usenp.random.seed(112)random_descriptions = np.random.choice(descriptions, 1000, replace=False)res = call_llama('You are a product categorization assistant at a retail website.','Given the following product descriptions, come up with a few product categories they should be classified into.'+'\n'.join(random_descriptions))categories = ['Home Decor','Kitchen and Dining','Fashion Accessories','Stationary and Gifts','Toys and Games','Seasonal and Holiday','Personal Care and Wellness','Outdoor and Garden', ]print(res['generation'])

['JUMBO BAG PINK POLKADOT', 'BLUE POLKADOT WRAP', 'RED RETROSPOT WRAP ', 'RECYCLING BAG RETROSPOT ', 'RED RETROSPOT SHOPPER BAG']

<<SYS>>Based on the product descriptions, I would categorize them into the following categories:

1. Home Decor:

* Wall art

* Decorative items (e.g. vases, figurines, etc.)

* Lighting (e.g. candles, lanterns, etc.)

* Textiles (e.g. throw pillows, blankets, etc.)

2. Kitchen and Dining:

* Cookware and utensils

* Tableware (e.g. plates, cups, etc.)

* Kitchen decor (e.g. signs, magnets, etc.)

* Food and drink items (e.g. tea, coffee, etc.)

3. Fashion and Accessories:

* Jewelry (e.g. necklaces, earrings, etc.)

* Handbags and wallets

* Clothing and accessories (e.g. scarves, hats, etc.)

* Beauty and personal care items (e.g. cosmetics, skincare, etc.)

4. Stationery and Gifts:

* Greeting cards

* Gift wrap and bags

* Stationery (e.g. notebooks, pens, etc.)

* Gift items (e.g. mugs, keychains, etc.)

5. Toys and Games:

* Toys (e.g. stuffed animals, puzzles, etc.)

* Games and puzzles

* Outdoor toys and games

6. Seasonal and Holiday:

* Christmas decorations and gifts

* Easter decorations and gifts

* Halloween decorations and gifts

* Other seasonal and holiday items

7. Office and School:

* Office supplies (e.g. pens, paper, etc.)

* School supplies (e.g. backpacks, lunchboxes, etc.)

* Desk accessories (e.g. paperweights, etc.)

8. Garden and Outdoor:

* Gardening tools and supplies

* Outdoor decor (e.g. planters, etc.)

* Patio and outdoor furniture

9. Baby and Kids:

* Baby clothing and accessories

* Kids' clothing and accessories

* Toys and games for kids

* Nursery decor and furniture

Note that some products may fit into multiple categories, but I've tried to categorize them based on their primary function or theme.

Code

#loop through descriptions in batches of batch_sizeres_texts = []batch_size =100for i in tqdm(range(0, len(descriptions), batch_size)): batch = descriptions[i:i+batch_size] d ="\n".join(batch) inp =f'''Categorize the following product descriptions into {", ".join(categories)} or Others, if they do not fall into any. Only answer in the following format:"product description of product #1"|"product category classified into""product description of product #2"|"product category classified into"..."product description of product #n"|"product category classified into"Here are the product descriptions:{d}'''whileTrue: res = call_claude('You are a product categorizer at a retail website', inp)# if res['generation_token_count'] > 1: #for llamaif res['usage']['output_tokens'] >1:breakelse:print('Retrying...') time.sleep(2) res_text = res['content'][0]['text'].strip().split('\n')#for llama# .replace('[SYS]','').replace('<<SYS>>','')\# .replace('[/SYS]','').replace('<</SYS>>','')\if res_text!='': res_texts.extend(res_text)withopen('../../data/sales_prediction/product_description_category.csv','w') as f: f.write('"product_description"|"category"\n')for i in res_texts: f.write(f'{i}\n')

Here is the share of product descriptions in each annotated category:

category

Home Decor 0.328636

Kitchen and Dining 0.195885

Fashion Accessories 0.138670

Stationary and Gifts 0.116122

Seasonal and Holiday 0.087373

Personal Care and Wellness 0.047351

Toys and Games 0.045096

Outdoor and Garden 0.032976

Others 0.007892

Name: proportion, dtype: float64

We merge the RFM features with preference features, that is share of sales in each category for every customer, then the outcome TargetSales to create the universe set for the problem.

Code

feature_transaction_cat = feature_transaction.merge(product_description_category, how='inner', on ='Description',)feature_transaction.shape, feature_transaction_cat.shape#convert invoice date to datetimefeature_transaction_cat['InvoiceDate'] = pd.to_datetime(feature_transaction_cat['InvoiceDate'])# last date in feature setcurrent_date = feature_transaction_cat['InvoiceDate'].max()#rfmcustomer_features = feature_transaction_cat.groupby('CustomerID').agg({'InvoiceDate': [ ('recency', lambda x: (current_date - x.max()).days), ('first_purchase_date', 'min'), ('purchase_day', 'nunique'), ],'InvoiceNo': [('nb_invoice', 'nunique')],'Sales': [ ('total_sales', 'sum') ],'StockCode': [('nb_product', 'nunique')],'category': [('nb_category', 'nunique')]}).reset_index()# Flatten column namescustomer_features.columns = ['CustomerID','recency','first_purchase_date','purchase_day','nb_invoice','total_sales','nb_product','nb_category']customer_features['customer_lifetime'] = (current_date - customer_features['first_purchase_date']).dt.dayscustomer_features['avg_purchase_frequency'] = customer_features['customer_lifetime'] / customer_features['purchase_day']customer_features['avg_purchase_value'] = customer_features['total_sales'] / customer_features['purchase_day']#category preferencecategory_sales = feature_transaction_cat.pivot_table( values='Sales', index='CustomerID', columns='category', aggfunc='sum', fill_value=0)category_sales.columns = [i.lower().replace(' ','_') for i in category_sales.columns]customer_features = customer_features.merge(category_sales, on='CustomerID', how='left')total_sales = customer_features['total_sales']for col in category_sales.columns: percentage_col =f'per_{col}' customer_features[percentage_col] = customer_features[col] / total_salesselected_features = ['recency','purchase_day','total_sales','nb_product','nb_category','customer_lifetime','avg_purchase_frequency','avg_purchase_value','per_fashion_accessories','per_home_decor','per_kitchen_and_dining','per_others','per_outdoor_and_garden','per_personal_care_and_wellness','per_seasonal_and_holiday','per_stationary_and_gifts','per_toys_and_games']outcome_variable ='TargetSales'customer_features = customer_features[[ 'CustomerID']+selected_features]df = outcome_df.merge(customer_features, on='CustomerID').drop('CustomerID', axis=1)print(df.shape)df.sample(5)

(3438, 18)

TargetSales

recency

purchase_day

total_sales

nb_product

nb_category

customer_lifetime

avg_purchase_frequency

avg_purchase_value

per_fashion_accessories

per_home_decor

per_kitchen_and_dining

per_others

per_outdoor_and_garden

per_personal_care_and_wellness

per_seasonal_and_holiday

per_stationary_and_gifts

per_toys_and_games

2606

0.00

53

2

597.48

138

8

184

92.000000

298.740

0.079383

0.433973

0.343710

0.003465

0.000000

0.041357

0.016570

0.056688

0.024854

196

0.00

78

2

2209.85

37

6

226

113.000000

1104.925

0.030771

0.275245

0.628549

0.000000

0.021178

0.022535

0.000000

0.021721

0.000000

2900

3893.79

10

6

4099.11

78

9

172

28.666667

683.185

0.003879

0.761507

0.104540

0.003879

0.012442

0.014015

0.051597

0.043312

0.004830

2187

0.00

227

1

122.40

1

1

227

227.000000

122.400

0.000000

0.000000

1.000000

0.000000

0.000000

0.000000

0.000000

0.000000

0.000000

322

0.00

68

1

147.12

3

2

68

68.000000

147.120

0.881729

0.118271

0.000000

0.000000

0.000000

0.000000

0.000000

0.000000

0.000000

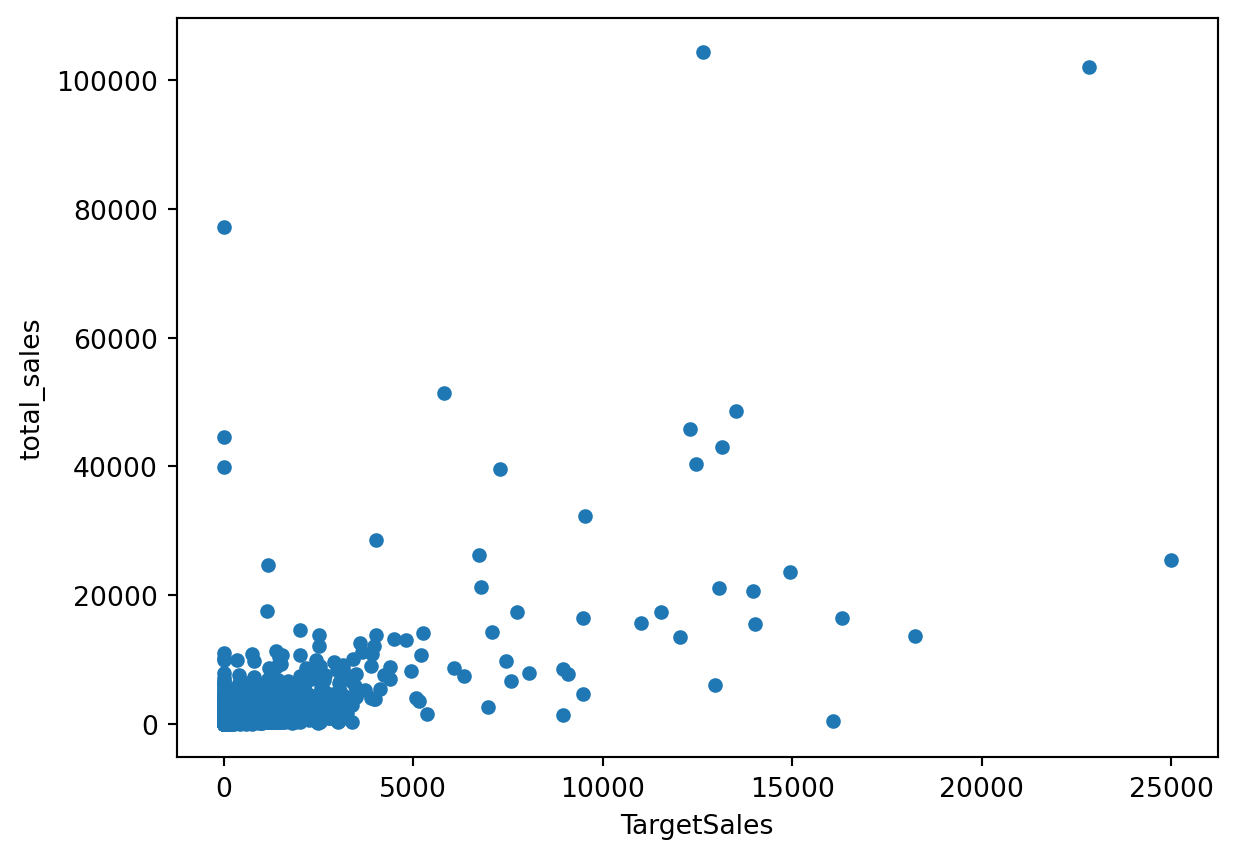

Univariate correlation expectedly pinpoints total_sales in during Q1-Q3 2011 as the most predictive feature; however, we can see that it is still not very predictive. This shows that the problem is not a trivial one.

Code

print(df[['TargetSales','total_sales']].corr())#target and most predictive variabledf[df.TargetSales<=25_000].plot.scatter(x='TargetSales',y='total_sales')

We randomly split the dataset into train and test sets at 80/20 ratio. We also confirm the distribution of TargetSales is similar across percentiles between train and test and only different at the upper end.

Code

#split into train-valid setstrain_df, test_df = train_test_split(df, test_size=0.2, random_state=112)pd.concat([train_df.TargetSales.describe(percentiles=[i/10for i inrange(10)]).reset_index(),test_df.TargetSales.describe(percentiles=[i/10for i inrange(10)]).reset_index(),], axis=1)

index

TargetSales

index

TargetSales

0

count

2750.000000

count

688.000000

1

mean

642.650436

mean

760.558808

2

std

4015.305436

std

4024.524400

3

min

0.000000

min

0.000000

4

0%

0.000000

0%

0.000000

5

10%

0.000000

10%

0.000000

6

20%

0.000000

20%

0.000000

7

30%

0.000000

30%

0.000000

8

40%

0.000000

40%

0.000000

9

50%

91.350000

50%

113.575000

10

60%

260.308000

60%

277.836000

11

70%

426.878000

70%

418.187000

12

80%

694.164000

80%

759.582000

13

90%

1272.997000

90%

1255.670000

14

max

168469.600000

max

77099.380000

Naive Baseline Regression

The most naive solution is to simply predict TargetSales based on the features. We use a stacked ensemble of LightGBM, CatBoost, XGBoost, Random Forest and Extra Trees via AutoGluon. We train with good_quality preset, stated to be “Stronger than any other AutoML Framework”, for speedy training and inference but feel free to try more performant options. We exclude the neural-network models as they require further preprocessing of the features. We use an industry-grade, non-parametric model to be as close to a real use case as possible and make a point that the methodology works not only in a toy-dataset setup.

An alternative approach to deal with long/fat-tailed outcome is to train on a winsorized outcome. In our case, we cap the outlier at 99.0% or TargetSales equals 7,180.81. While this solves the long/fat-tailed issues, it does not deal with zero inflation and also introduce bias to the outcome. This leads to better performance when tested on the winsorized outcome, but not so much on the original outcome.

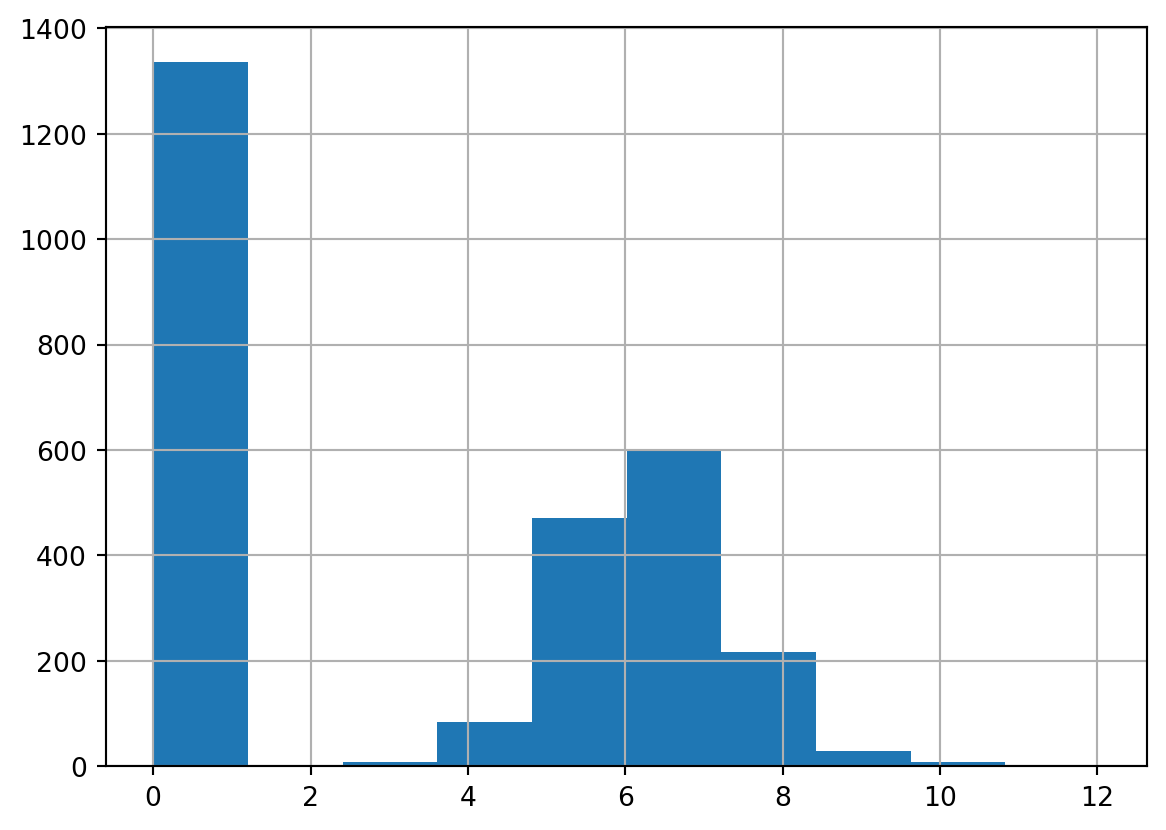

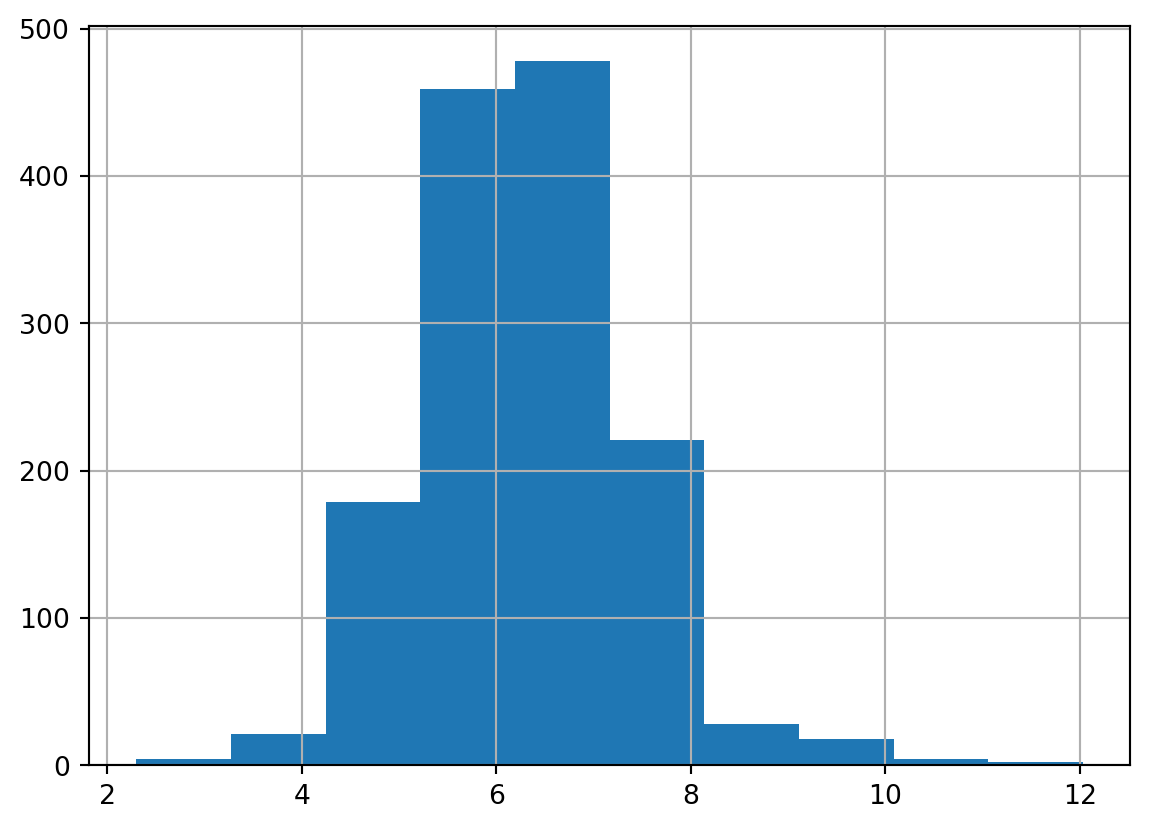

Log transformation handles long/fat-tailed distribution and is especially useful for certain models since the transformed distribution is closer normal. However, it cannot handle zero-valued outcome and oftentimes scientists end up adding 1 to the outcome (so often that numpy even has a function for it). This not only introduces bias to the prediction, but also does not solve the zero-inflation as it becomes one-inflation instead.

Code

#logtrain_df['TargetSales_log1p'] = train_df['TargetSales'].map(np.log1p)test_df['TargetSales_log1p'] = test_df['TargetSales'].map(np.log1p)#from zero-inflated to one-inflatedtrain_df['TargetSales_log1p'].hist()

We can see that this is the best performing approach so far, which is one of the reasons why so many scientists end up going for this not-entirely-correct approach.

Hurdle model is a two-stage approach that handles zero inflation by first having a classification model to predict if the outcome is zero or not, then a regression model, trained only on examples with actual non-zero outcomes, to fit a log-transformed outcome. When retransforming the predictions from log to non-log numbers, we perform correction of underestimation using Duan’s method. During inference time, we multiply the predictions from the classification and corrected regression model.

For our splits, 51.42% of train and 53.05% of test include customers with non-zero purchase outcome. As with all two-stage approaches, we need to make sure the intermediate model performs reasonably in classifying zero/non-zero outcomes.

After that, we perform log-transformed regression on the examples with non-zero outcome (1,414 examples in train). Without the need to worry about ln(0) outcome, the regression is much more straightforward albeit with fewer examples to train on.

For inference, we combine the binary prediction (purchase/no purchase) from the classification model with the re-transformed (exponentialized) numerical prediction from the regression model by simply multiplying them together. As you can see, this approach yields the best performance so far and this is where I used to think everything has been accounted for.

In the previous section, we have blissfully assumed that we can freely log-transform and re-transform the outcome during training and inference without any bias. This is not the case as there is a small bias generated in the process due to the error term.

The average treatment affect (ATE; \(E[y]\)) is underestimated by \(E[exp(\epsilon)]\). Naihua Duan (段乃華), a Taiwanese biostatistician, suggested a consistent estimator of \(E[exp(\epsilon)]\) in his 1983 work as

\(\hat \lambda\) is the Duan’s smearing estimator of the bias from re-transformation \(E[exp(\epsilon)]\)

\(\hat y\) is the prediction aka \(f(X)\)

Fun Fact: If you assume Duan were a western name, you would have been

pronouncing the method's name incorrectly since it should be [twàn]'s

method, NOT /dwɑn/'s method.

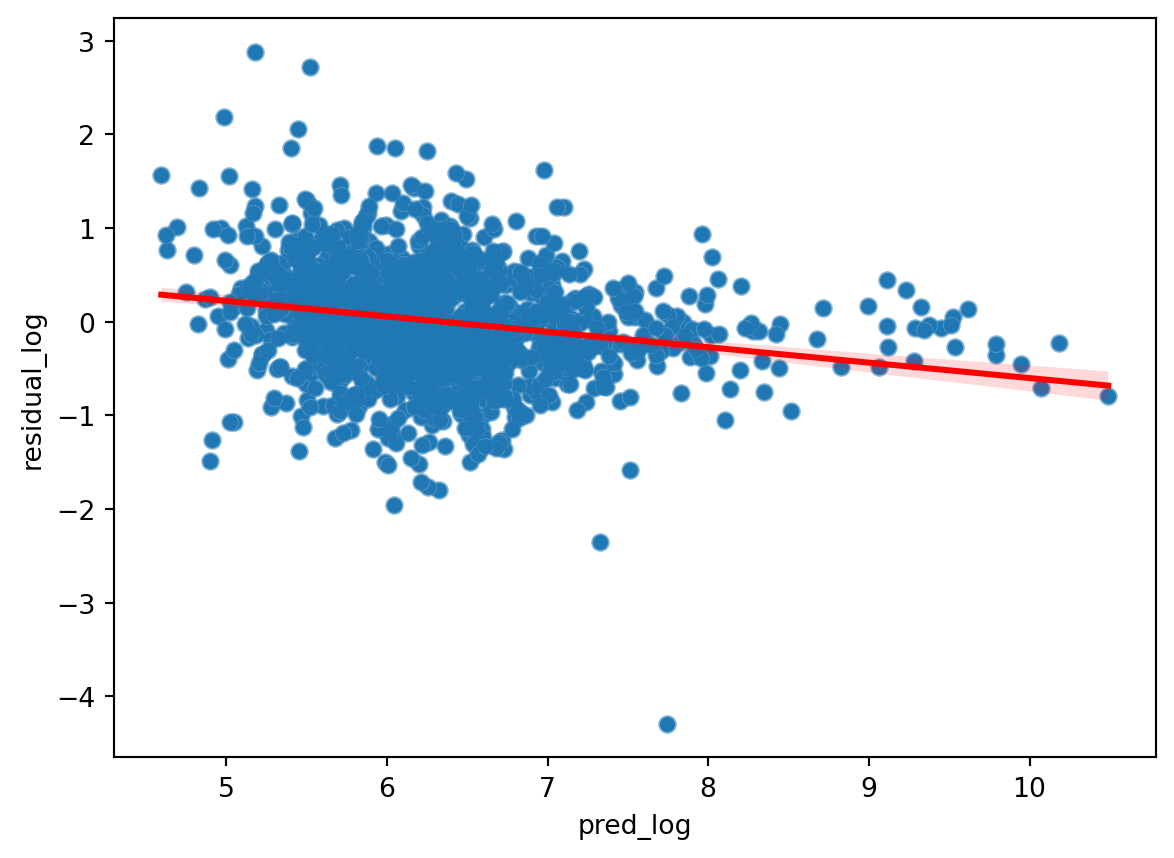

Before we proceed, the formulation of Duan’s smearing estimator assumes that estimates of error terms (residuals) for log predictions be independent and identically distributed. Since we are dealing with individual customers, independence can be assumed. However, if we look at the plot of residuals vs predicted log values (based on training set), we can see that they do not look particularly identically distributed.

Code

#plot residual and predicted log valuetrain_df_nonzero['pred_log'] = predictor_reg.predict(train_df_nonzero[selected_features])train_df_nonzero['residual_log'] = (train_df_nonzero['pred_log'] - train_df_nonzero['TargetSales_log'])# Create the scatter plotsns.scatterplot(x='pred_log', y='residual_log', data=train_df_nonzero)# Add the Lowess smoothing linesns.regplot(x='pred_log', y='residual_log', data=train_df_nonzero, scatter_kws={'alpha': 0.5}, line_kws={'color': 'red'})

Although note that White test does not reject the null hypothesis of the residuals being homoscedastic in reference to the features. This counterintuitive result might stem from the fact that White test is assuming linear or quadratic relationships between outcome and features while the residuals are derived from a stacked ensemble of decision trees.

White Test Statistic: 129.31318320644837

P-value: 0.8761278601130765

Our choice is to either trust the White test and pretend assume everything is fine; or trust our eyes and replace the non-zero regression model with one that produces iid residuals such as generalized least squares (GLS) with heteroscedasticity-robust standard errors. The tradeoff is that often models that produce homoscedastic residuals perform worse in terms of predictive power (see example of GLS implementation in Assumption on Indepedent and Identically Distributed Residuals section of the notebook).

Assuming we trust the White test, we can easily derive Duan’s smearing estimator by taking mean of error between actual and predicted TargetSales in the training set.

We can see that the hurdle model with Duan’s correction performs best across majority of the metrics. We will now deep dive on metrics where it did not to understand the caveats when taking this approach.

Code

metric_df = pd.DataFrame([metric_baseline, metric_winsorized, metric_log1p, metric_hurdle, metric_hurdle_corrected,])rank_df = metric_df.copy()for col in metric_df.columns.tolist()[:-1]:if col in ['r2', 'pearsonr', 'spearmanr']: rank_df[f'{col}_rank'] = rank_df[col].rank(ascending=False)else: rank_df[f'{col}_rank'] = rank_df[col].rank(ascending=True)rank_df = rank_df.drop(metric_df.columns.tolist()[:-1], axis=1)rank_df['avg_rank'] = rank_df.iloc[:,1:].mean(axis=1)rank_df.transpose()

0

1

2

3

4

model

baseline

winsorized

log1p

hurdle

hurdle_corrected

root_mean_squared_error_rank

2.0

4.0

5.0

3.0

1.0

mean_squared_error_rank

2.0

4.0

5.0

3.0

1.0

mean_absolute_error_rank

5.0

4.0

3.0

1.0

2.0

r2_rank

2.0

4.0

5.0

3.0

1.0

pearsonr_rank

3.0

5.0

4.0

1.5

1.5

spearmanr_rank

5.0

4.0

1.0

2.5

2.5

median_absolute_error_rank

5.0

3.0

1.0

2.0

4.0

earths_mover_distance_rank

3.0

4.0

5.0

2.0

1.0

avg_rank

3.375

4.0

3.625

2.25

1.75

Code

metric_df.transpose()

0

1

2

3

4

root_mean_squared_error

3162.478744

3623.576378

3725.342296

3171.760745

3055.320787

mean_squared_error

10001271.807776

13130305.763947

13878175.221577

10060066.223275

9334985.110424

mean_absolute_error

715.644266

627.788007

618.976847

584.916293

613.394664

r2

0.381617

0.188147

0.141906

0.377981

0.422813

pearsonr

0.619072

0.575799

0.581717

0.67697

0.67697

spearmanr

0.470085

0.504302

0.533816

0.510708

0.510708

median_absolute_error

232.982083

219.622481

89.554954

199.178014

232.555574

earths_mover_distance

287.777288

432.128843

581.049444

286.381443

241.618399

model

baseline

winsorized

log1p

hurdle

hurdle_corrected

Why Duan’s Correction Results in Slightly Worse MAE?

Duan’s method adjusts for underestimation from re-transformation of log outcome. This could lead to smaller extreme errors, but more frequent occurrences of less extreme ones. We verify this hypothesis by comparing mean absolute error before and after transformation for errors originally under and over 99th percentile. We confirm that is the case for our problem.

Code

err_hurdle = (test_df['TargetSales'] - test_df['pred_hurdle']).abs()err_hurdle_corrected = (test_df['TargetSales'] - test_df['pred_hurdle_corrected']).abs()print('Distribution of errors for Hurdle model without correction')err_hurdle.describe(percentiles=[.25, .5, .75, .9, .95, .99])

Distribution of errors for Hurdle model without correction

count 688.000000

mean 584.916293

std 3119.628924

min 0.000000

25% 0.000000

50% 199.178014

75% 475.603446

90% 862.530026

95% 1237.540954

99% 6763.777844

max 55731.205996

dtype: float64

Code

print('Hurdle Model without correction')print(f'Mean absolute error under 99th percentile: {err_hurdle[err_hurdle<6763.777844].mean()}')print(f'Mean absolute error over 99th percentile: {err_hurdle[err_hurdle>6763.777844].mean()}')print('Hurdle Model with correction')print(f'Mean absolute error under 99th percentile: {err_hurdle_corrected[err_hurdle<6763.777844].mean()}')print(f'Mean absolute error over 99th percentile: {err_hurdle_corrected[err_hurdle>6763.777844].mean()}')

Hurdle Model without correction

Mean absolute error under 99th percentile: 355.4918014848842

Mean absolute error over 99th percentile: 22904.641872667555

Hurdle Model with correction

Mean absolute error under 99th percentile: 392.7718802742851

Mean absolute error over 99th percentile: 22076.839798471465

Importance of Classification Model

The overperformance of log-transform regression over both hurdle model approarches in Spearman’s rank correlation and median absolute error demonstrates the importance of a classification model. At first glance, it is perplexing since we have just spent a large portion of this article to justify that hurdle models handle zero inflation better and re-transformation without Duan’s method is biased. However, it becomes clear once you compare performance of the hurdle model with a classification model (f1 = 0.69) and a hypothetical, perfect classification model. Other metrics also improved but not nearly as drastic as MedAE and Spearman’s rank correlation.

One last thing to remember is that we are trying to predict sales of each individual customer, not total sales of all customers. If we look at aggregated mean or sum of actual sales vs predicted sales, baseline regression performs best by far. This is due to the fact that without any constraints a regressor only minimizes the MSE loss and usually ends up predicting values around the mean to balance between under- and over-predictions. However, this level of prediction is often not very useful as a single point. Imagine you want to give promotions with higher or lower spend thresholds to customers according to their purchasing power; you will not be able to do so with a model that is accurate on aggregate but not so much on individual customers.

And this is how you predict how much a customer will spend in the least wrong way. My hope is that you will not need to spend ten years in data science to find out how to do it like I did.